Your credit score, debt, and monthly budget all play a big role in getting a mortgage. This guide explains everything in simple terms so you know what to focus on before you buy a home.

What Is a Credit Score?

A credit score is a number that shows how well you handle money and debt. Most scores range from 300 to 850.

Higher scores make it easier to get approved for a mortgage and can help you get a lower interest rate.

Quick breakdown:

720+ = Excellent

680–719 = Good

620–679 = Fair

Below 620 = Needs work

Your credit score is one of the biggest factors in getting a mortgage.

How to Improve Your Credit Score

Here are easy ways to raise your score before applying for a mortgage:

Pay bills on time

Keep credit card balances low

Don’t open new accounts unless needed

Pay down debt slowly over time

Check your credit report for mistakes

Small changes make a big difference.

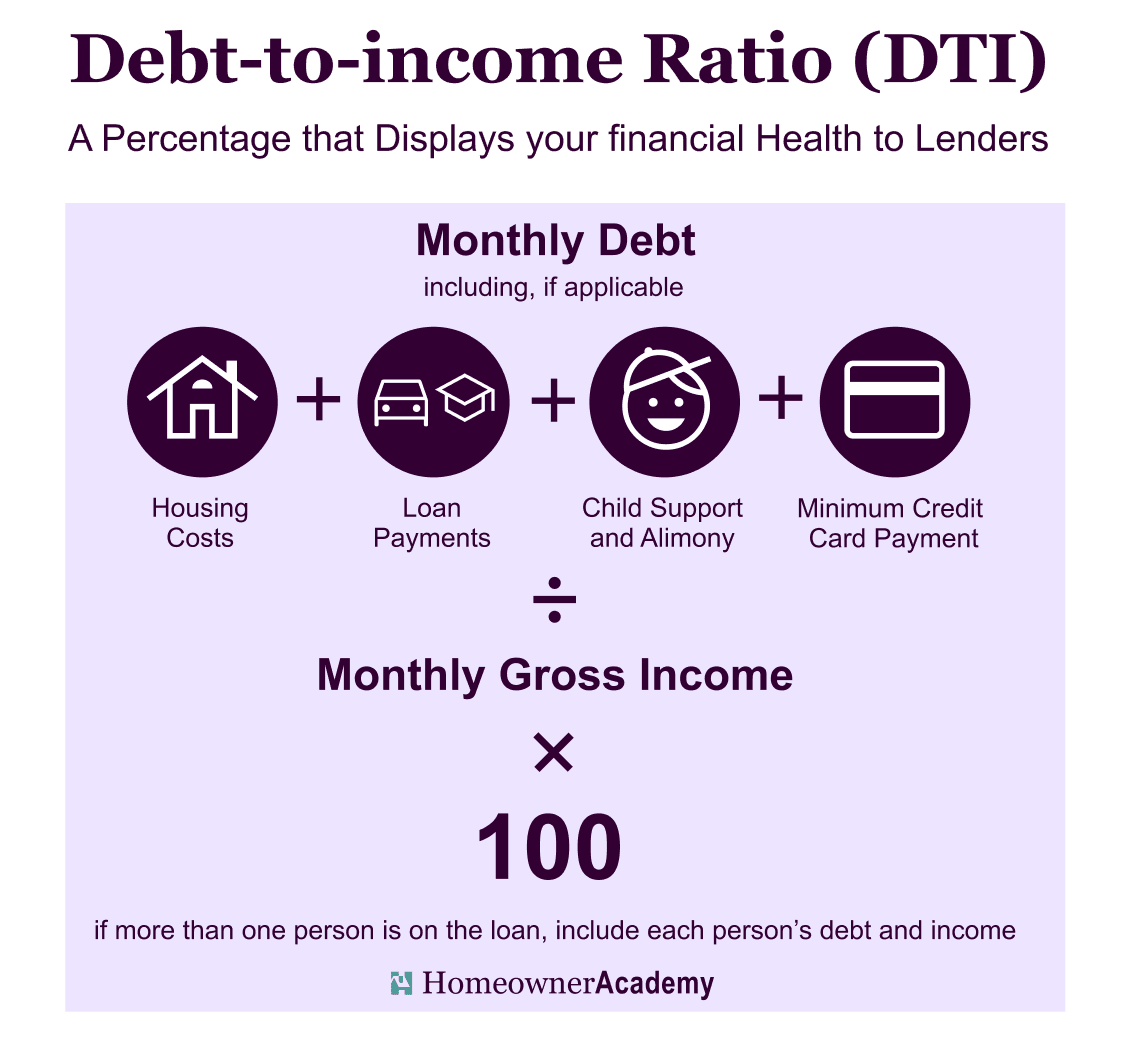

What Is a Debt-to-Income Ratio (DTI)?

Your DTI compares how much money you make to how much you owe each month.

Formula: Monthly debt ÷ Monthly income x 100 = DTI

Examples of monthly debt:

Car payments

Student loans

Credit card payments

Personal loans

Minimum required payments

Most lenders want a DTI of 43% or lower. Lower DTI = better chance of getting approved.

How Much House Can You Afford?

A simple rule many first-time buyers use:

Your total monthly home payment should be around 25%–30% of your monthly income.

Your home payment includes:

Mortgage

Taxes

Insurance

(Sometimes) HOA fees

(Sometimes) PMI

This helps make sure your budget stays comfortable.

How to Build a Budget for Buying a Home

Use this simple plan to get started:

List your monthly income

List your monthly bills and debts

Plan for savings

Add room for home expenses

Decide how much you can comfortably spend on a monthly payment

Budgeting helps you know when you’re ready and what price range fits your life.

How to Save Money for a Home

Here are small steps that help over time:

Set a monthly savings goal

Put savings in a separate account

Track spending for one month

Use cash-back or rewards programs

Put bonuses or tax refunds into savings

Cut 1–2 small expenses (subscriptions, eating out, etc.)

You don’t need to save everything at once — small steps build up.

How Credit and Budget Affect Your Mortgage

Both matter for different reasons:

Credit score affects your interest rate and loan approval

DTI affects how much you can borrow

Budget helps you choose the right home payment

Savings affects your down payment and closing costs

Improving even one of these can make the whole homebuying process easier.

Summary

Your credit, debt, and monthly budget all work together when buying a home. You don’t need perfect credit or huge savings — you just need a clear plan. Focus on improving your score, lowering your debt, and building a simple budget to stay on track.

Explore more guides in the Buying Basics and Mortgages sections, or try the Home Readiness Check™ to see where you stand today.